Spurstow Parish Council’s income includes an Annual Precept that is taken from an element of each parishoner’s Council Tax bill. This is then paid semi-annually to the Parish Council and used to cover such costs as insurance, lighting, Clerk’s salary, general maintenance etc. The Parish Lengthsman was formerly funded through a separate grant from Cheshire East Council.

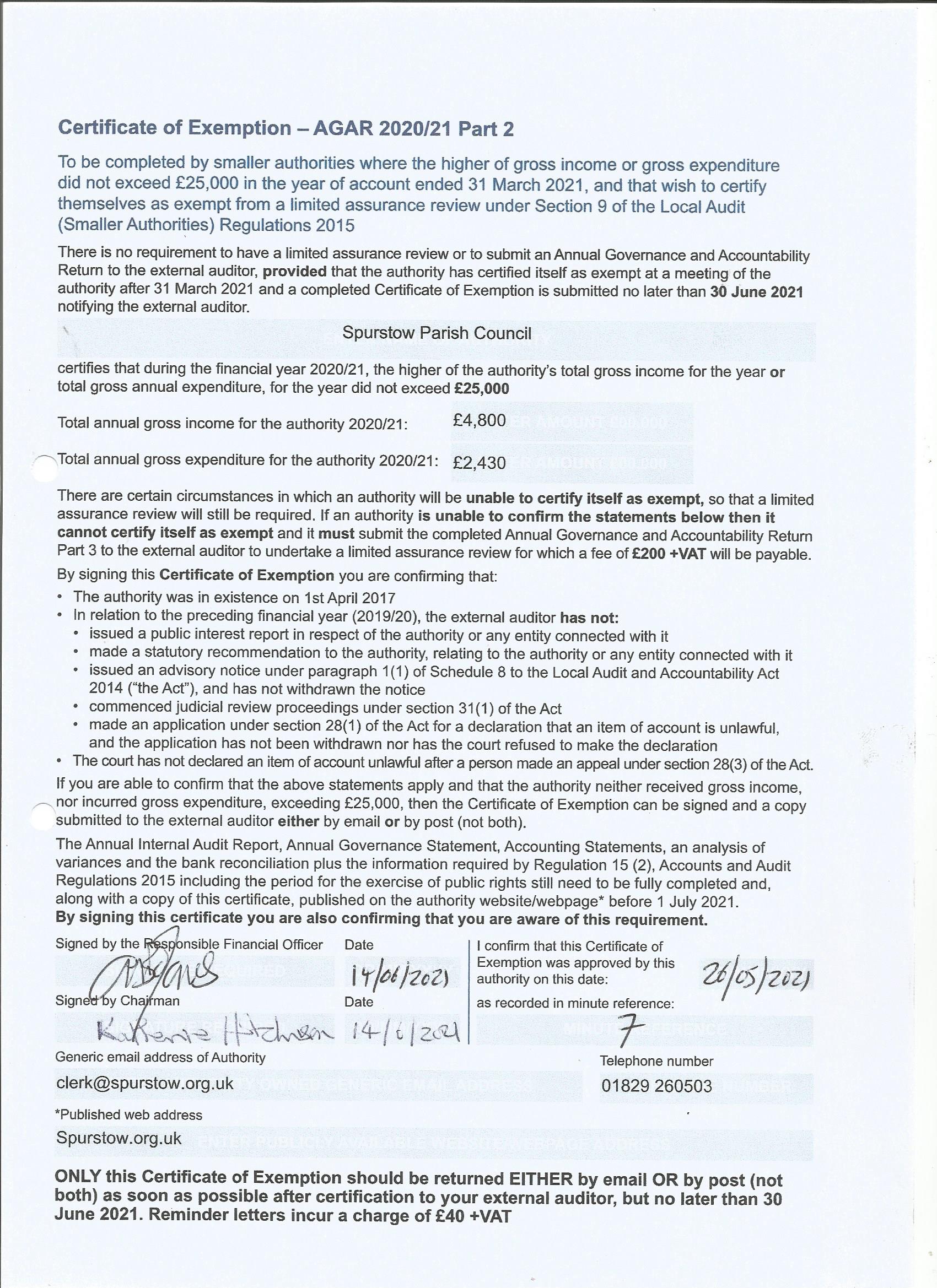

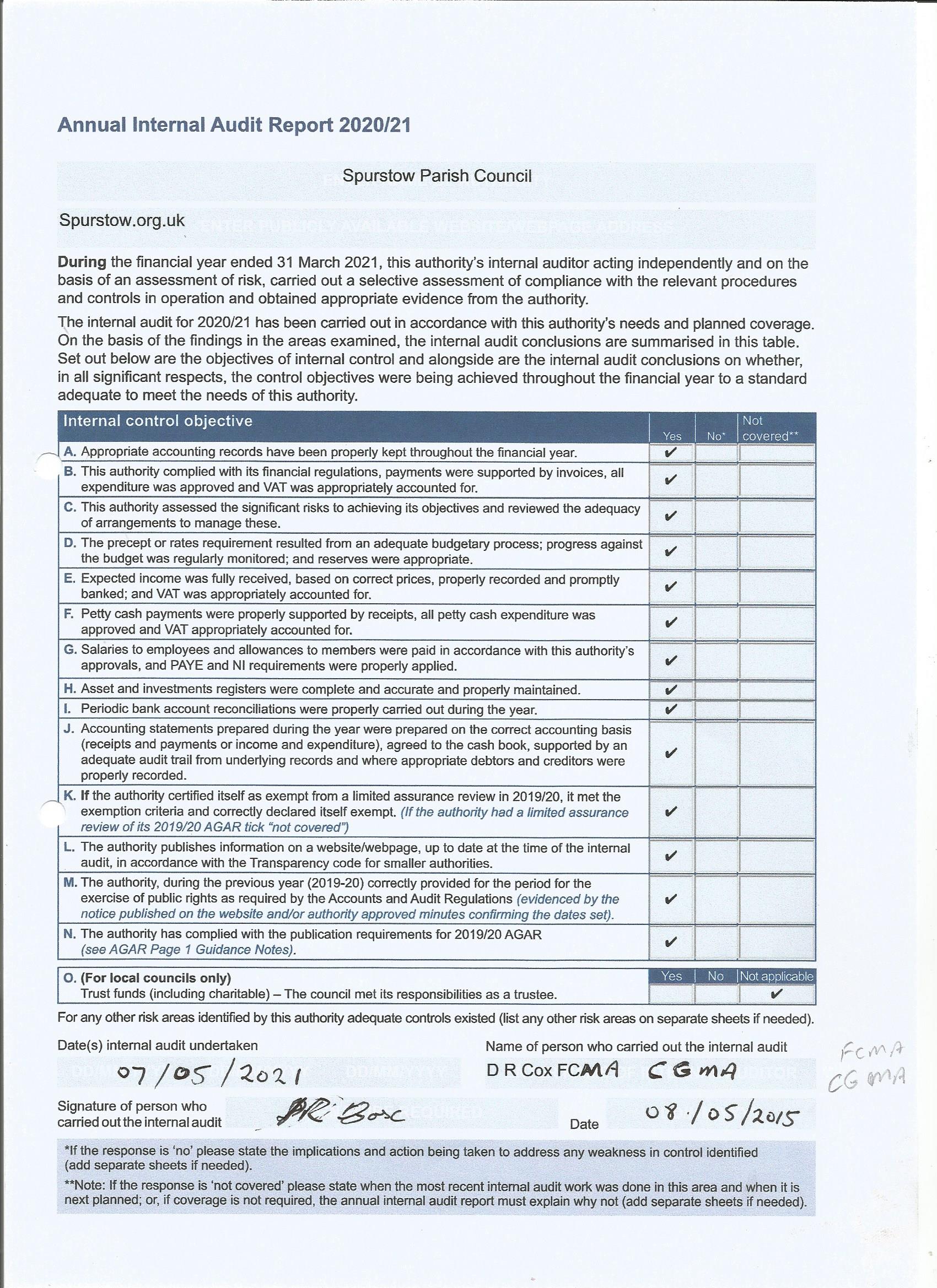

The Accounts are audited every year and are available for the public to inspect, via the Clerk. Please refer to the Council Governance page for further information.

Please click on the links below for the Council’s Annual Governance and Accountability Returns and supporting Documents.

2024-2025 Documentation

Spurstow Parish Council

NOTICE OF PUBLIC RIGHTS AND PUBLICATION OF ANNUAL GOVERNANCE & ACCOUNTABILITY RETURN (EXEMPT AUTHORITY)

ACCOUNTS FOR THE YEAR ENDED 31 MARCH 2025

Local Audit and Accountability Act 2014 Sections 25, 26 and 27

The Accounts and Audit Regulations 2015 (SI 2015/234)

1. Date of announcement 30th June 2025

2. Each year the smaller authority prepares an Annual Governance and Accountability Return (AGAR). The AGAR has been published with this notice. It will not be reviewed by the appointed auditor, since the smaller authority has certified itself as exempt from the appointed auditor’s review.

Any person interested has the right to inspect and make copies of the AGAR, the accounting records for the financial year to which it relates and all books, deeds, contracts, bills, vouchers, receipts and other documents relating to those records must be made available for inspection by any person interested. For the year ended 31 March 2024, these documents will be available on reasonable notice by application to: C M B Jones, Clerk to Spurstrow Parish Council, Rose Cottage, Peckforton Hall Lane, Spurstow, CW6 9TG clerk@spurstow.org.uk

commencing on 1st July 2025 and ending on 9th August 2025

3. Local government electors and their representatives also have:

The opportunity to question the appointed auditor about the accounting records; and

The right to make an objection which concerns a matter in respect of which the appointed auditor could either make a public interest report or apply to the court for a declaration that an item of account is unlawful. Written notice of an objection must first be given to the auditor and a copy sent to the smaller authority.

The appointed auditor can be contacted at the address in paragraph 4 below for this purpose between the above dates only.

4. The smaller authority’s AGAR is only subject to review by the appointed auditor if questions or objections raised under the Local Audit and Accountability Act 2014 lead to the involvement of the auditor. The appointed auditor is:

PKF Littlejohn LLP (Ref: SBA Team)

15 Westferry Circus

Canary Wharf

London E14 4HD

5. This announcement is made by CM B Jones, Clerk to Spurstow Parish Council

https://www.spurstow.org.uk/wp-content/uploads/Spurstow-Parish-Council-AGAR-2024-2025.docx

2023-2024 Documentation

Spurstow Parish Council

NOTICE OF PUBLIC RIGHTS AND PUBLICATION OF ANNUAL GOVERNANCE & ACCOUNTABILITY RETURN (EXEMPT AUTHORITY)

ACCOUNTS FOR THE YEAR ENDED 31 MARCH 2024

Local Audit and Accountability Act 2014 Sections 25, 26 and 27

The Accounts and Audit Regulations 2015 (SI 2015/234)

1. Date of announcement 29th June 2024

2. Each year the smaller authority prepares an Annual Governance and Accountability Return (AGAR). The AGAR has been published with this notice. It will not be reviewed by the appointed auditor, since the smaller authority has certified itself as exempt from the appointed auditor’s review.

Any person interested has the right to inspect and make copies of the AGAR, the accounting records for the financial year to which it relates and all books, deeds, contracts, bills, vouchers, receipts and other documents relating to those records must be made available for inspection by any person interested. For the year ended 31 March 2024, these documents will be available on reasonable notice by application to: C M B Jones, Clerk to Pecforton Parish Meeting, Rose Cottage, Peckforton Hall Lane, Spurstow, CW6 9TG peckfortonparishclerk@gmail.com

commencing on Monday 1st July 2024 and ending on 9th August 2024

3. Local government electors and their representatives also have:

The opportunity to question the appointed auditor about the accounting records; and

The right to make an objection which concerns a matter in respect of which the appointed auditor could either make a public interest report or apply to the court for a declaration that an item of account is unlawful. Written notice of an objection must first be given to the auditor and a copy sent to the smaller authority.

The appointed auditor can be contacted at the address in paragraph 4 below for this purpose between the above dates only.

4. The smaller authority’s AGAR is only subject to review by the appointed auditor if questions or objections raised under the Local Audit and Accountability Act 2014 lead to the involvement of the auditor. The appointed auditor is:

PKF Littlejohn LLP (Ref: SBA Team)

15 Westferry Circus

Canary Wharf

London E14 4HD

5. This announcement is made by CM B Jones, Clerk to Peckforton Parish Meeting.

https://www.spurstow.org.uk/wp-content/uploads/Spurstow-AGAR-2023-2024-Page-1.pdf

https://www.spurstow.org.uk/wp-content/uploads/Spurstow-AGAR-2023-2024-Page-2.pdf

https://www.spurstow.org.uk/wp-content/uploads/Spurstow-AGAR-2023-2024-Page-3.pdf

https://www.spurstow.org.uk/wp-content/uploads/Spurstow-AGAR-2023-2024-Page-4.pdf

https://www.spurstow.org.uk/wp-content/uploads/Spurstow-AGAR-2023-2024-Page-5.pdf

https://www.spurstow.org.uk/wp-content/uploads/Spurstow-AGAR-2023-2024-Page-6.pdf

2022-2023 Documentation

Spurstow Parish Council

NOTICE OF PUBLIC RIGHTS AND PUBLICATION OF ANNUAL GOVERNANCE & ACCOUNTABILITY RETURN (EXEMPT AUTHORITY)

ACCOUNTS FOR THE YEAR ENDED 31 MARCH 2023

Local Audit and Accountability Act 2014 Sections 25, 26 and 27

The Accounts and Audit Regulations 2015 (SI 2015/234)

| NOTICE |

| 1. Date of announcement 22th May 2023 2. Each year the smaller authority prepares an Annual Governance and Accountability Return (AGAR). The AGAR has been published with this notice. It will not be reviewed by the appointed auditor, since the smaller authority has certified itself as exempt from the appointed auditor’s review. Any person interested has the right to inspect and make copies of the AGAR, the accounting records for the financial year to which it relates and all books, deeds, contracts, bills, vouchers, receipts and other documents relating to those records must be made available for inspection by any person interested. For the year ended 31 March 2023, these documents will be available on reasonable notice by application to: C Jones, Clerk to Peckforton Parish Meeting, by email to Clerk@spurstow.org.uk or call 01829 260503. commencing on Monday 5th June 2023 ending on Friday 14th July 2023 3. Local government electors and their representatives also have: The opportunity to question the appointed auditor about the accounting records; andThe right to make an objection which concerns a matter in respect of which the appointed auditor could either make a public interest report or apply to the court for a declaration that an item of account is unlawful. Written notice of an objection must first be given to the auditor and a copy sent to the smaller authority. The appointed auditor can be contacted at the address in paragraph 4 below for this purpose between the above dates only. 4. The smaller authority’s AGAR is only subject to review by the appointed auditor if questions or objections raised under the Local Audit and Accountability Act 2014 lead to the involvement of the auditor. The appointed auditor is: PKF Littlejohn LLP (Ref: SBA Team) 15 Westferry Circus Canary Wharf London E14 4HD (sba@pkf-l.com) 5. This announcement is made by C Jones, Clerk to Peckforton Parish Meeting |

LOCAL AUTHORITY ACCOUNTS: A SUMMARY OF YOUR RIGHTS

Please note that this summary applies to all relevant smaller authorities, including parish meetings where there is no parish council.

The basic position

The Local Audit and Accountability Act 2014 (the Act) governs the work of auditors appointed to smaller authorities. This summary explains the provisions contained in Sections 26 and 27 of the Act. The Act and the Accounts and Audit Regulations 2015 also cover the duties, responsibilities and rights of smaller authorities, other organisations and the public concerning the accounts being audited.

As a local elector, or an interested person, you have certain legal rights in respect of the accounting records of smaller authorities. As an interested person you can inspect accounting records and related documents. If you are a local government elector for the area to which the accounts relate you can also ask questions about the accounts and object to them. You do not have to pay directly for exercising your rights. However, any resulting costs incurred by the smaller authority form part of its running costs. Therefore, indirectly, local residents pay for the cost of you exercising your rights through their council tax.

The right to inspect the accounting records

Any interested person can inspect the accounting records, which includes but is not limited to local electors. You can inspect the accounting records for the financial year to which the audit relates and all books, deeds, contracts, bills, vouchers, receipts and other documents relating to those records. You can copy all, or part, of these records or documents. Your inspection must be about the accounts, or relate to an item in the accounts. You cannot, for example, inspect or copy documents unrelated to the accounts, or that include personal information (Section 26 (6) – (10) of the Act explains what is meant by personal information). You cannot inspect information which is protected by commercial confidentiality. This is information which would prejudice commercial confidentiality if it was released to the public and there is not, set against this, a very strong reason in the public interest why it should nevertheless be disclosed.

When smaller authorities have finished preparing accounts for the financial year and approved them, they must publish them (including on a website). There must be a 30 working day period, called the ‘period for the exercise of public rights’, during which you can exercise your statutory right to inspect the accounting records. Smaller authorities must tell the public, including advertising this on their website, that the accounting records and related documents are available to inspect. By arrangement you will then have 30 working days to inspect and make copies of the accounting records. You may have to pay a copying charge. The 30 working day period must include a common period of inspection during which all smaller authorities’ accounting records are available to inspect. This will be 3-14 July 2023 for 2022/23 accounts. The advertisement must set out the dates of the period for the exercise of public rights, how you can communicate to the smaller authority that you wish to inspect the accounting records and related documents, the name and address of the auditor, and the relevant legislation that governs the inspection of accounts and objections.

The right to ask the auditor questions about the accounting records

You should first ask your smaller authority about the accounting records, since they hold all the details. If you are a local elector, your right to ask questions of the external auditor is enshrined in law. However, while the auditor will answer your questions where possible, they are not always obliged to do so. For example, the question might be better answered by another organisation, require investigation beyond the auditor’s remit, or involve disproportionate cost (which is borne by the local taxpayer). Give your smaller authority the opportunity first to explain anything in the accounting records that you are unsure about. If you are not satisfied with their explanation, you can question the external auditor about the accounting records.

The law limits the time available for you formally to ask questions. This must be done in the period for the exercise of public rights, so let the external auditor know your concern as soon as possible. The advertisement or notice that tells you the accounting records are available to inspect will also give the period for the exercise of public rights during which you may ask the auditor questions, which here means formally asking questions under the Act. You can ask someone to represent you when asking the external auditor questions.

Before you ask the external auditor any questions, inspect the accounting records fully, so you know what they contain. Please remember that you cannot formally ask questions, under the Act, after the end of the period for the exercise of public rights. You may ask your smaller authority other questions about their accounts for any year, at any time. But these are not questions under the Act.

You can ask the external auditor questions about an item in the accounting records for the financial year being audited. However, your right to ask the external auditor questions is limited. The external auditor can only answer ‘what’ questions, not ‘why’ questions. The external auditor cannot answer questions about policies, finances, procedures or anything else unless it is directly relevant to an item in the accounting records. Remember that your questions must always be about facts, not opinions. To avoid misunderstanding, we recommend that you always put your questions in writing.

The right to make objections at audit

You have inspected the accounting records and asked your questions of the smaller authority. Now you may wish to object to the accounts on the basis that an item in them is in your view unlawful or there are matters of wider concern arising from the smaller authority’s finances. A local government elector can ask the external auditor to apply to the High Court for a declaration that an item of account is unlawful, or to issue a report on matters which are in the public interest. You must tell the external auditor which specific item in the accounts you object to and why you think the item is unlawful, or why you think that a public interest report should be made about it. You must provide the external auditor with the evidence you have to support your objection. Disagreeing with income or spending does not make it unlawful. To object to the accounts you must write to the external auditor stating you want to make an objection, including the information and evidence below and you must send a copy to the smaller authority. The notice must include:

- confirmation that you are an elector in the smaller authority’s area;

- why you are objecting to the accounts and the facts on which you rely;

- details of any item in the accounts that you think is unlawful; and

- details of any matter about which you think the external auditor should make a public interest report.

Other than it must be in writing, there is no set format for objecting. You can only ask the external auditor to act within the powers available under the Local Audit and Accountability Act 2014.

A final word

You may not use this ‘right to object’ to make a personal complaint or claim against your smaller authority. You should take such complaints to your local Citizens’ Advice Bureau, local Law Centre or to your solicitor. Smaller authorities, and so local taxpayers, meet the costs of dealing with questions and objections. In deciding whether to take your objection forward, one of a series of factors the auditor must take into account is the cost that will be involved, they will only continue with the objection if it is in the public interest to do so. They may also decide not to consider an objection if they think that it is frivolous or vexatious, or if it repeats an objection already considered. If you appeal to the courts against an auditor’s decision not to apply to the courts for a declaration that an item of account is unlawful, you will have to pay for the action yourself.

| For more detailed guidance on public rights and the special powers of auditors, copies of the publication Local authority accounts: A guide to your rights are available from the NAO website. | If you wish to contact your authority’s appointed external auditor please write to the address in paragraph 4 of the Notice of Public Rights and Publication of Unaudited Annual Governance & Accountability Return. |

Please find below the links to the Council’s Annual Governance and Accountability Return for the year to 31st March 2023

https://www.spurstow.org.uk/wp-content/uploads/Spurstow-AGAR-2022-2023-Page-1.jpeg

{kind=link}

https://www.spurstow.org.uk/wp-content/uploads/Spurstow-AGAR-2022-2023-Page-2.jpeg

{kind=link}

https://www.spurstow.org.uk/wp-content/uploads/Spurstow-AGAR-2022-2023-Page-3.jpeg

{kind=link}

https://www.spurstow.org.uk/wp-content/uploads/Spurstow-AGAR-2022-2023-Page-4.jpeg

{kind=link}

https://www.spurstow.org.uk/wp-content/uploads/Spurstow-AGAR-2022-2023-Page-5.jpeg

{kind=link}

https://www.spurstow.org.uk/wp-content/uploads/Spurstow-AGAR-2022-2023-Page-6.jpeg

{kind=link}

2021/22 Documentation

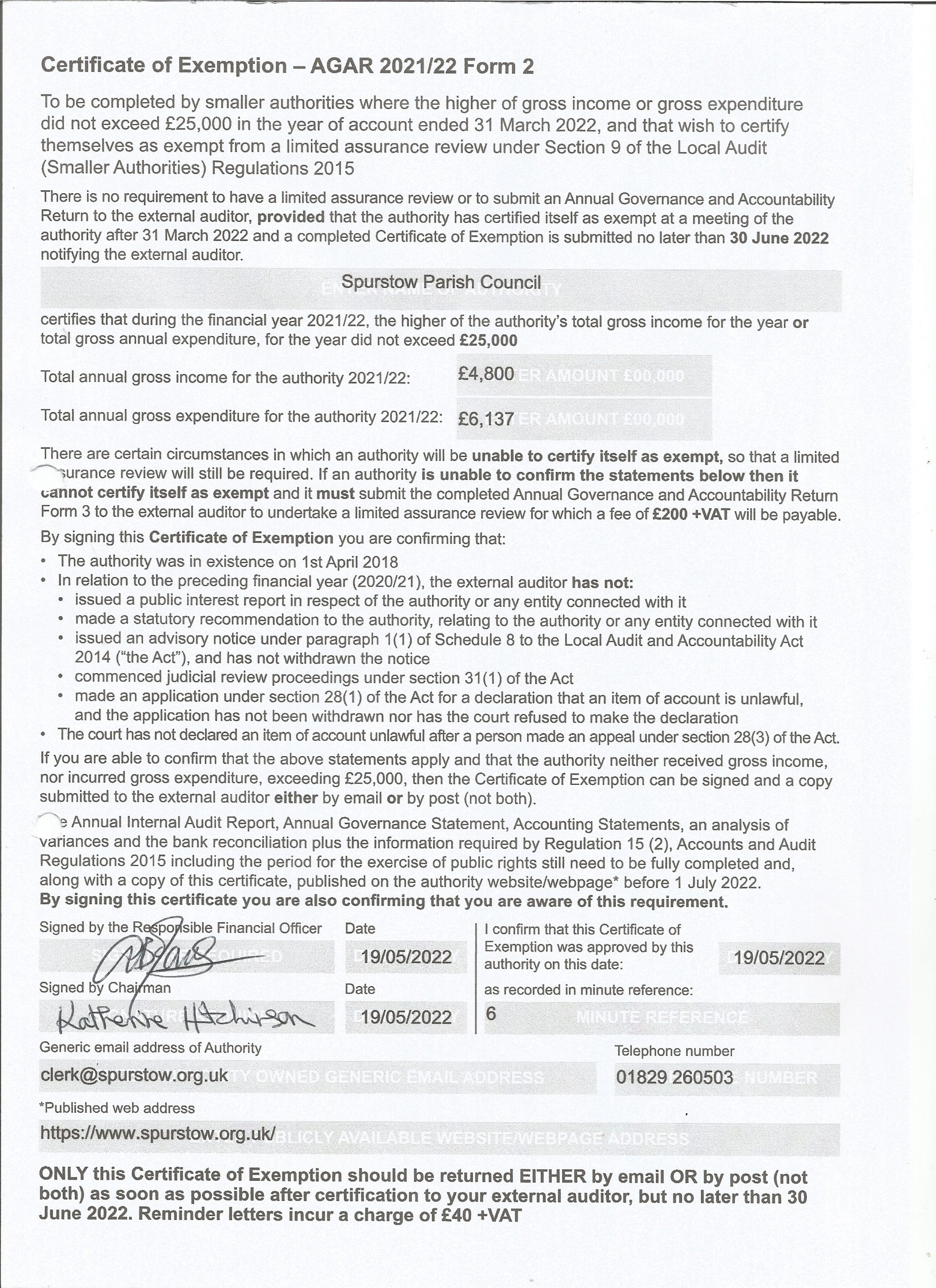

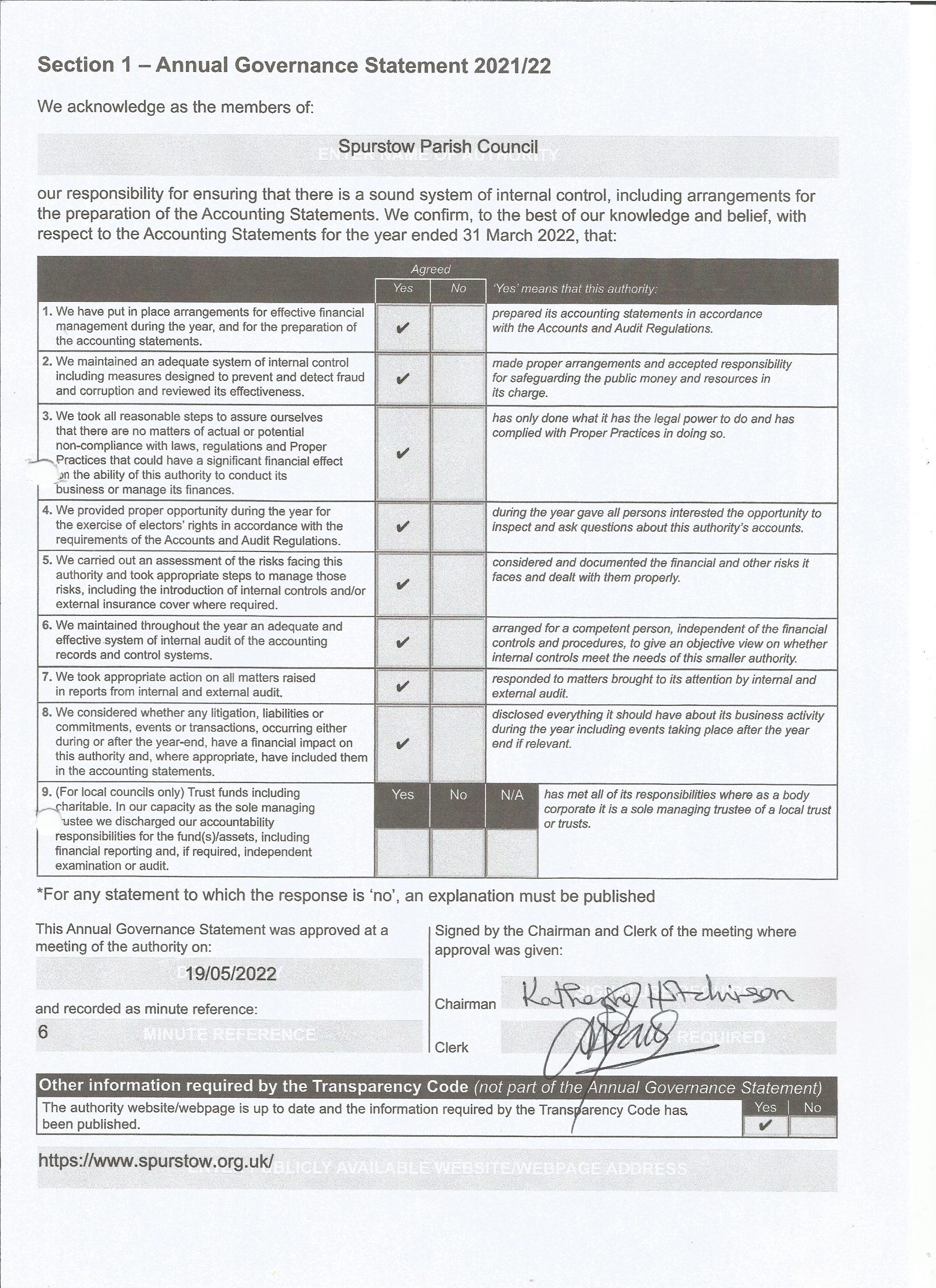

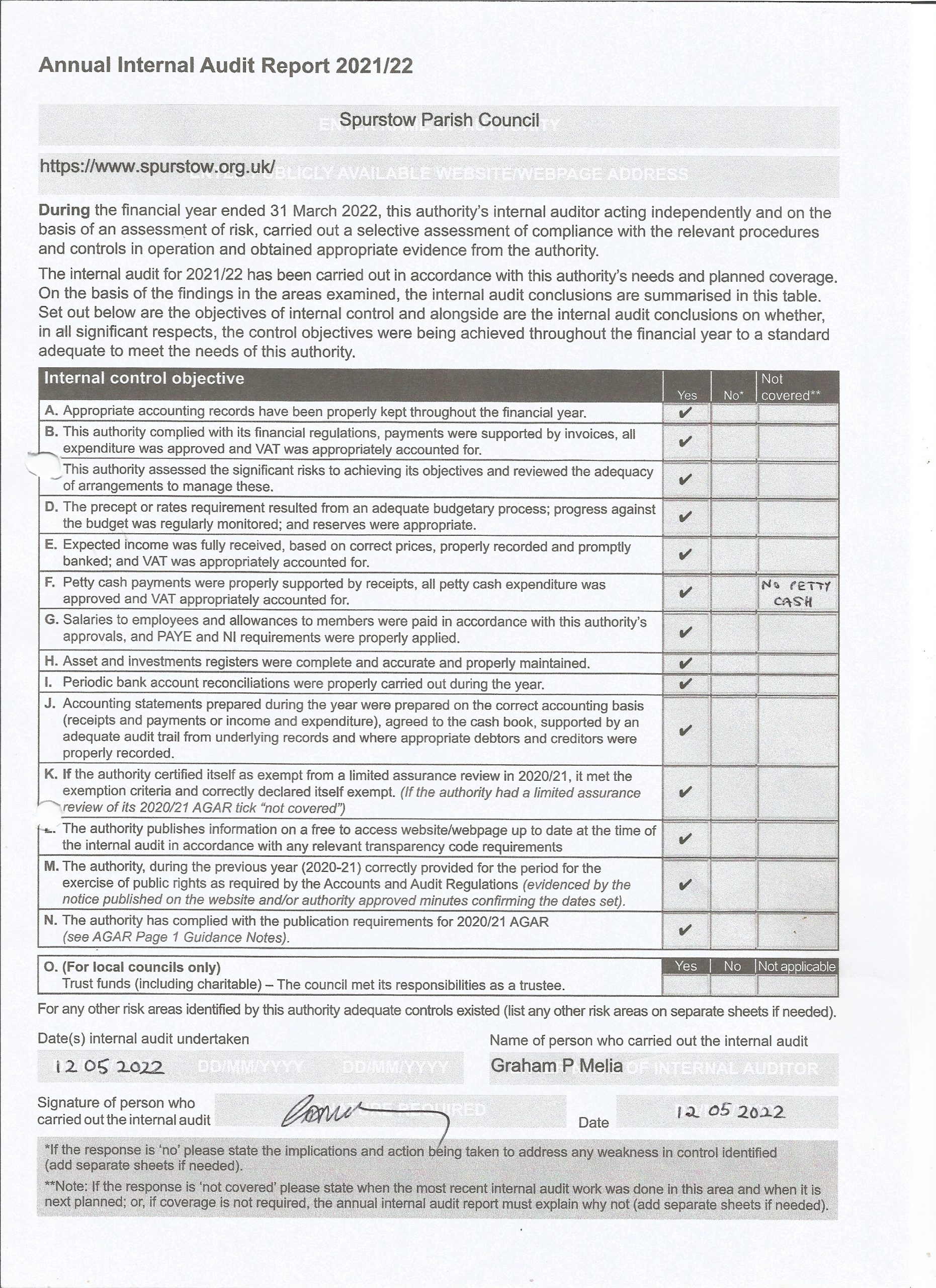

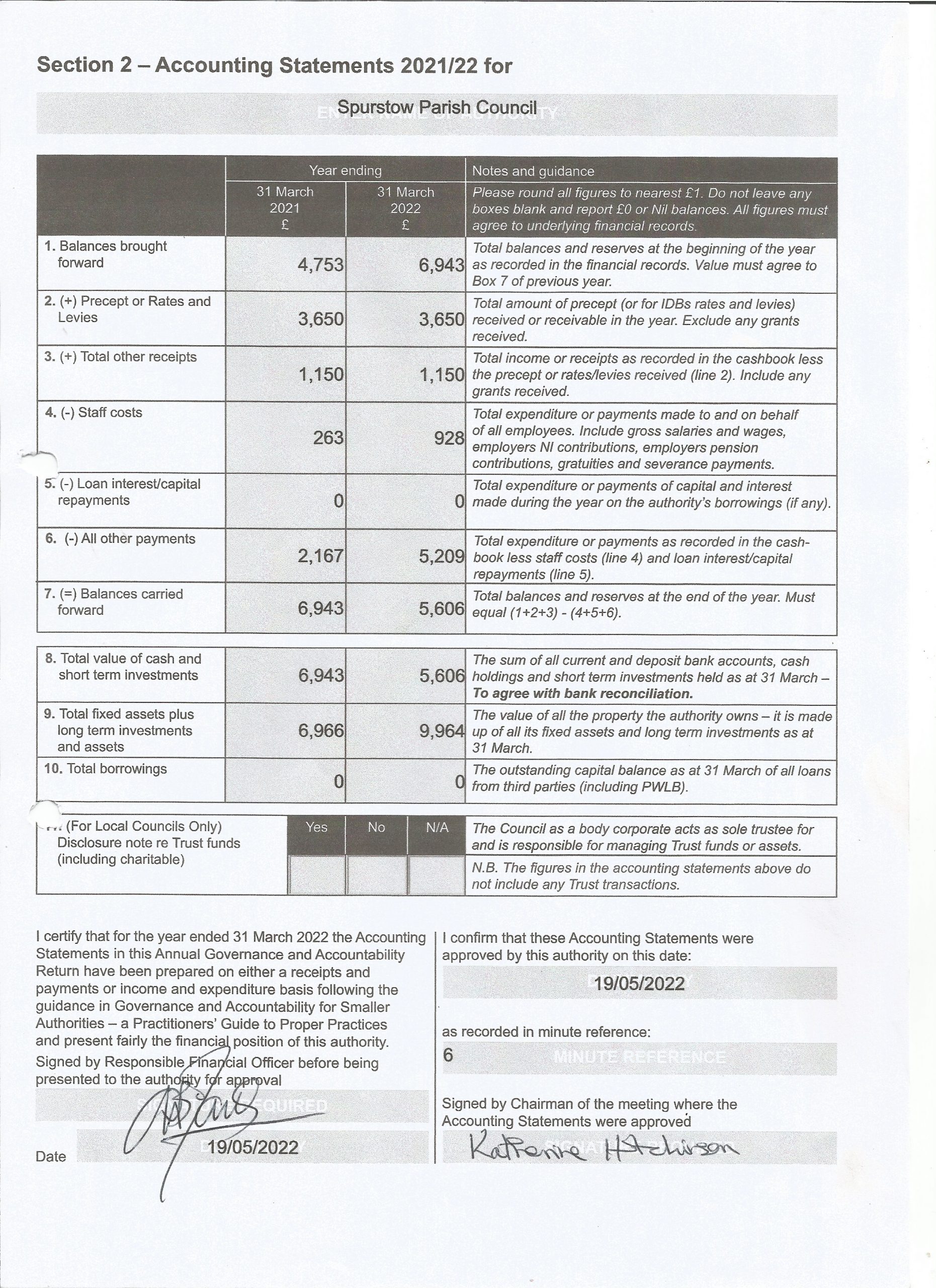

- https://www.spurstow.org.uk/wp-content/uploads/2021-22-AGAR-Page-1.jpeg

- https://www.spurstow.org.uk/wp-content/uploads/2021-22-AGAR-Page-2-scaled.jpeg

- https://www.spurstow.org.uk/wp-content/uploads/2021-22-AGAR-Page-3-scaled.jpeg

- https://www.spurstow.org.uk/wp-content/uploads/2021-22-AGAR-Page-4-scaled.jpeg

- https://www.spurstow.org.uk/wp-content/uploads/2021-22-AGAR-Page-5-scaled.jpeg

- https://www.spurstow.org.uk/wp-content/uploads/2021-22-AGAR-Page-6-scaled.jpeg

- Notice of public rights and publication of AGAR https://www.spurstow.org.uk/wp-content/uploads/Notice-of-Public-Rights-2021-2022.docx

- https://www.spurstow.org.uk/wp-content/uploads/Explanation-of-Variances-2021-2022-scaled.jpeg

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

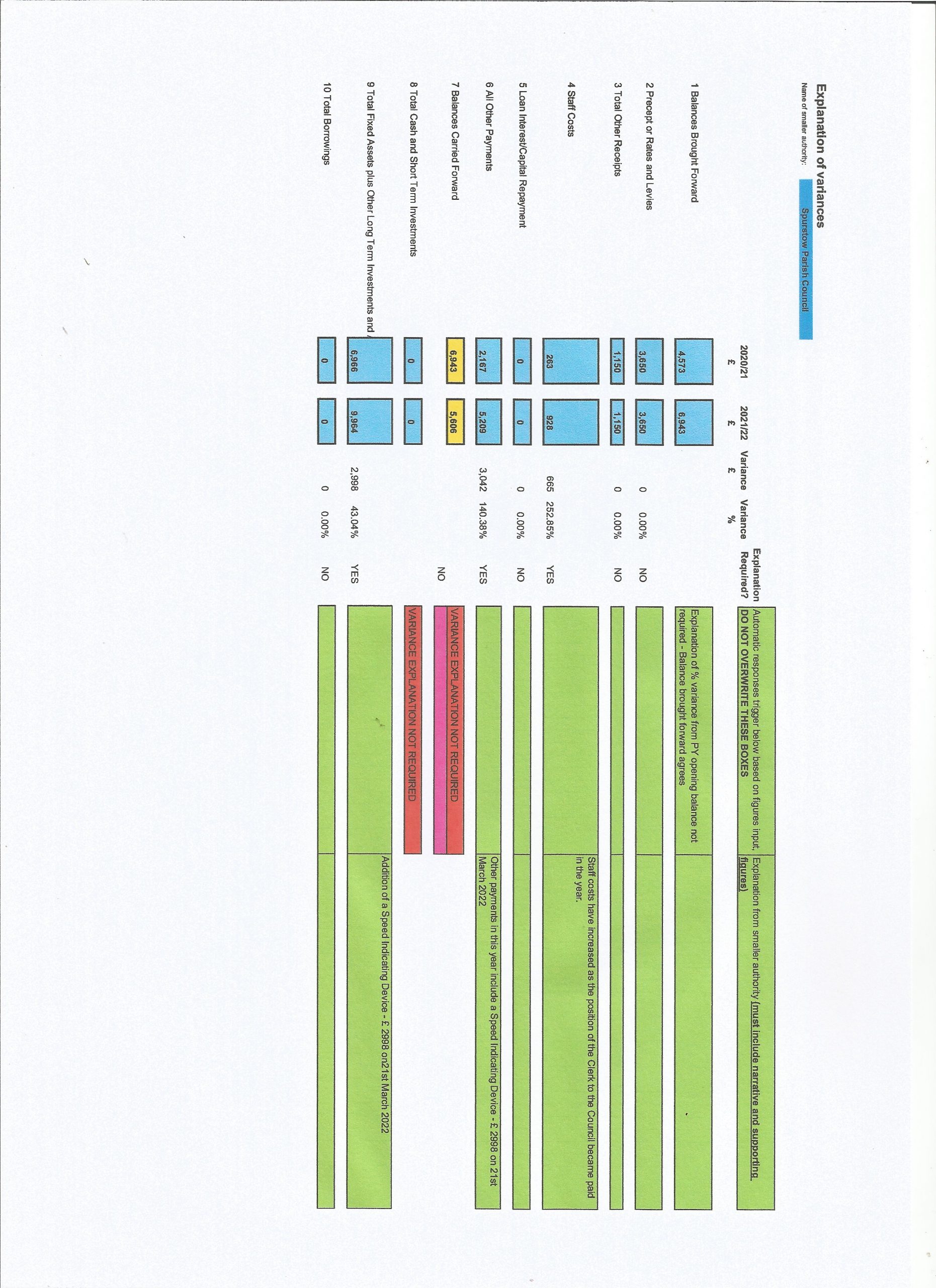

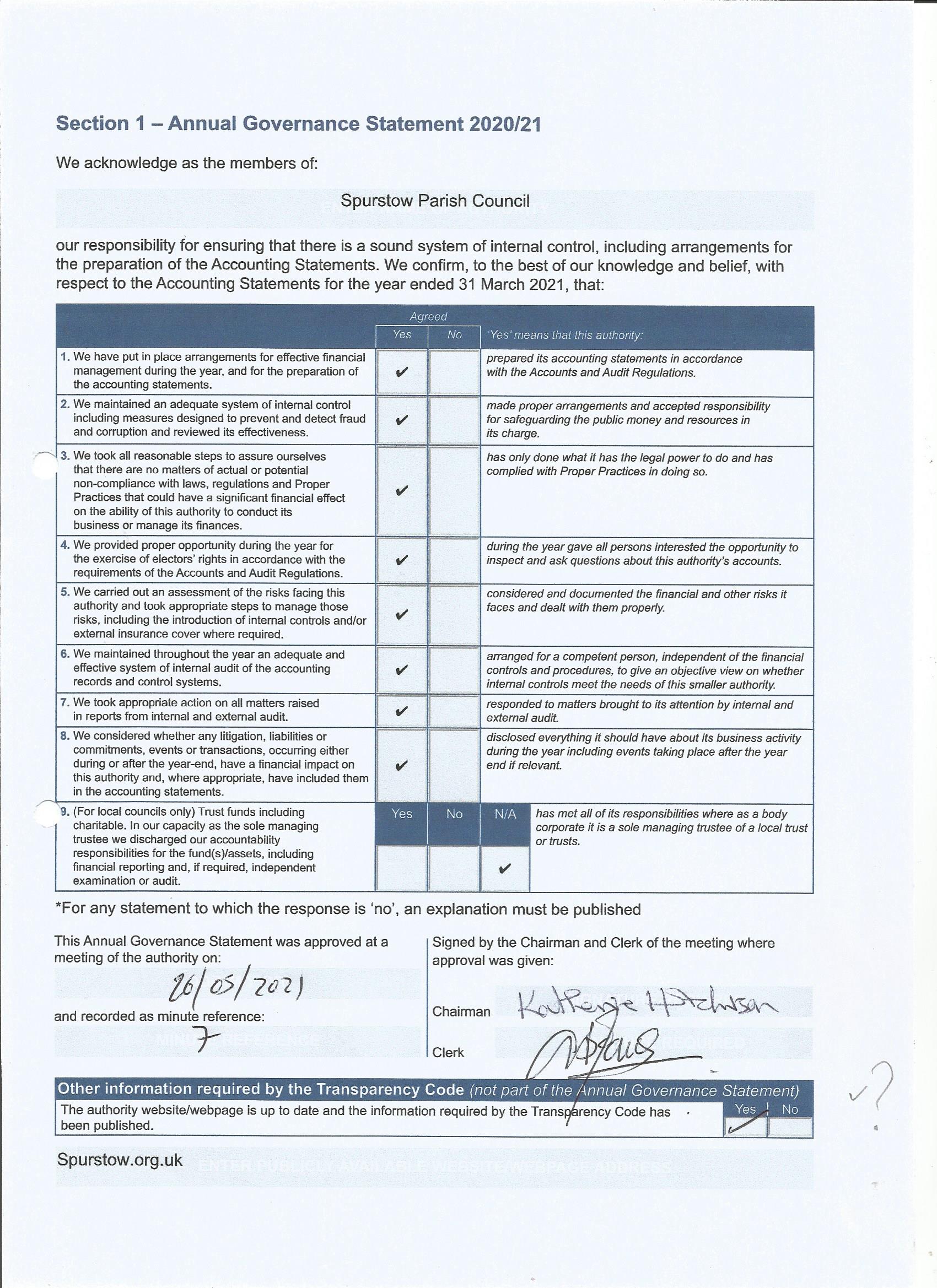

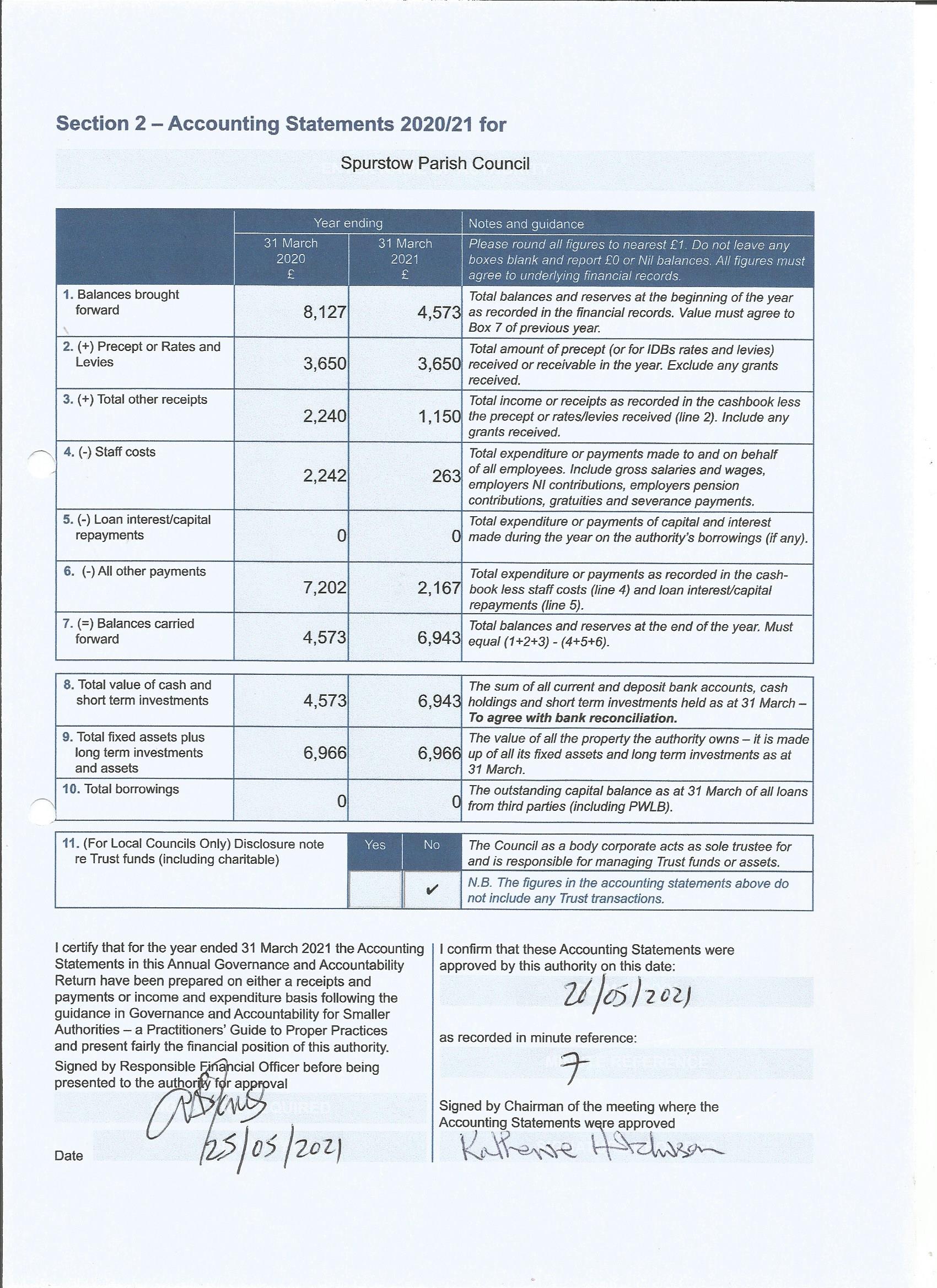

2020/21 Documentation

- Annual Governance and Accountability Return Page 1

- https://www.spurstow.org.uk/wp-content/uploads/AGAR-Page-2-Spurstow.jpeg

- https://www.spurstow.org.uk/wp-content/uploads/AGAR-Page-3-Spurstow.jpeg

- https://www.spurstow.org.uk/wp-content/uploads/AGAR-Page-4-Spurstow.jpeg

- https://www.spurstow.org.uk/wp-content/uploads/AGAR-Page-5-Spurstow.jpeg

- https://www.spurstow.org.uk/wp-content/uploads/AGAR-Page-6-Spurstow.jpeg

- Notice of public rights and publication of AGAR

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

2019/20 Documentation

- Annual Governance and Accountability Return

- Bank Reconciliation, Explanation of Variances, Asset Register and transaction details

- Notice of public rights and publication of AGAR

2018/19 Documentation

2017/18 Documentation

2016/17 Documentation

- 2016-17 accounts

- External Audit report 2016-17

- Notice of completed Audit 2016-17

- Exercise of Public rights 2016/17